At the Annual Meeting of the Greater Providence Chamber of Commerce, Providence, Rhode Island

Over the past year, my colleagues and I on the Federal Open Market Committee (FOMC) have been conducting a first-ever public review of how we make monetary policy. As part of that review, we held Fed Listens events around the country where representatives from a wide range of groups have been telling us how the economy is working for them and the people they represent and how the Federal Reserve might better promote the goals Congress has set for us: maximum employment and price stability. We have heard two messages loud and clear. First, as this expansion continues into its 11th year — the longest in U.S. history —economic conditions are generally good. Second, the benefits of the long expansion are only now reaching many communities, and there is plenty of room to build on the impressive gains achieved so far.

These themes show through in many ways in official statistics. For example, more than a decade of steady advances has pushed the jobless rate near a 50-year low, where it has remained for well over a year. But the wealth of middle-income families—savings, home equity, and other assets—has only recently surpassed levels seen before the Great Recession, and the wealth of people with lower incomes, while growing, has yet to fully recover.1

Fortunately, the outlook for further progress is good: Forecasters are generally predicting continued growth, a strong job market, and inflation near 2 percent. Tonight I will begin by discussing the Fed's policy actions over the past year to support the favorable outlook. Then I will turn to two important opportunities for further gains from this expansion: maintaining a stable and reliable pace of 2 percent inflation and spreading the benefits of employment more widely.

Monetary Policy and the Economy in 2019

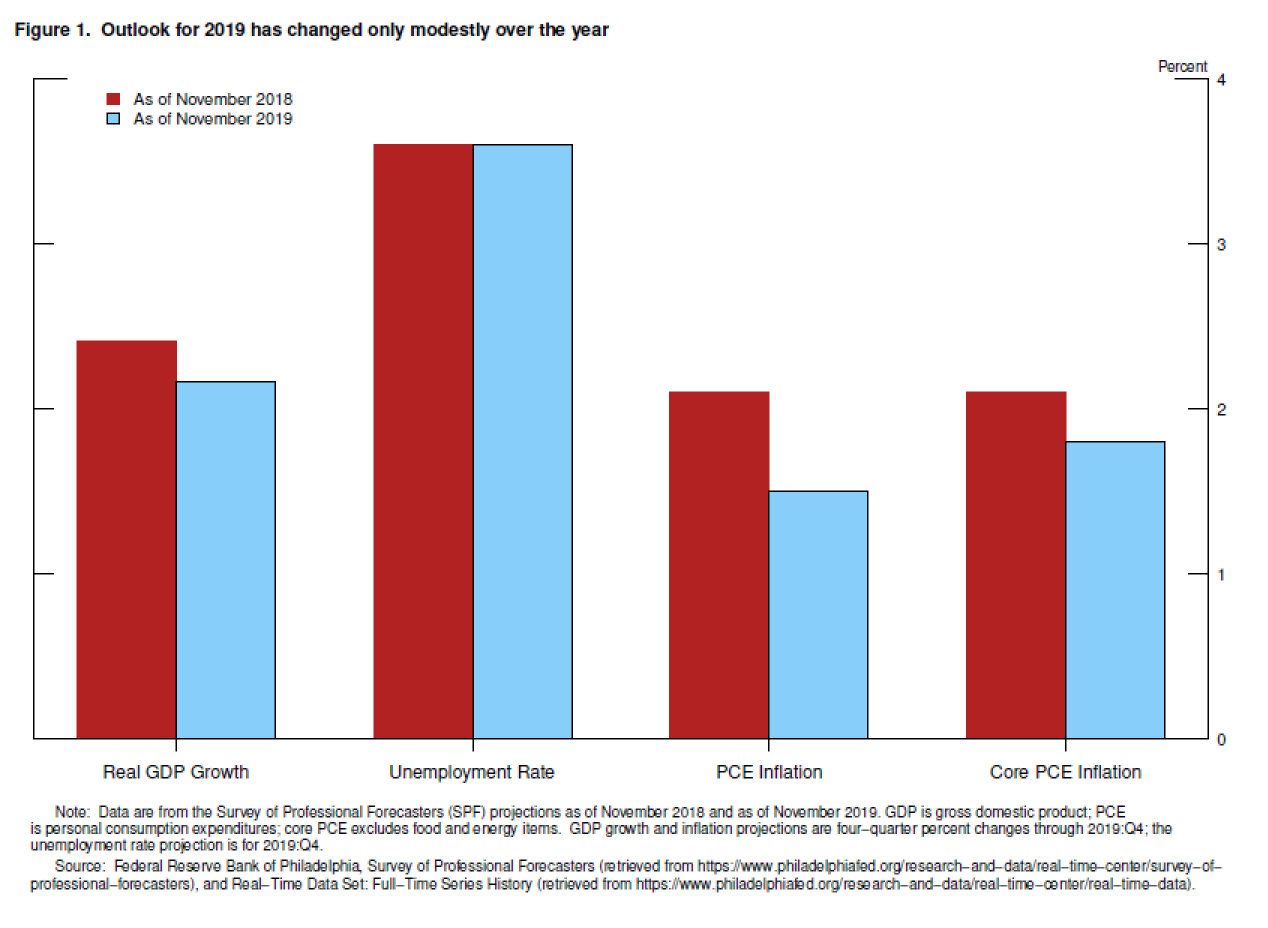

We started 2019 with a favorable outlook, and over the year the outlook has changed only modestly in the eyes of many forecasters (figure 1). For example, in the Survey of Professional Forecasters, the forecast for inflation is a bit lower, but the unemployment forecast is unchanged and the forecast for gross domestic product (GDP) is nearly unchanged.2 The key to the ongoing favorable outlook is household spending, which represents about 70 percent of the economy and continues to be strong, supported by the healthy job market, rising incomes, and solid consumer confidence.

{kind=link}

While events of the year have not much changed the outlook, the process of getting from there to here has been far from dull. I will describe how we grappled with incoming information and made important monetary policy changes through the year to help keep the favorable outlook on track.

More Articles

- November 1, 2023 Chair Jerome Powell’s Press Conference on Employment and Inflation

- Board of Governors of the Federal Reserve System: Something’s Got to Give by Governor Christopher J. Waller

- Jerome Powell's Semiannual Monetary Policy Report; Strong Wage Growth; Inflation, Labor Market, Unemployment, Job Gains, 2 Percent Inflation

- February’s Hot Data Releases: Governor Christopher J. Waller, Federal Reserve Board Frames a Few of the Issues Around Inflation and the Economic Outlook

- The Beige Book Summary of Commentary on Current Economic Conditions By Federal Reserve District Wednesday November 30, 2022

- Reflections on Monetary Policy in 2021 By Federal Reserve Governor Christopher J. Waller or "How did the Fed get so far behind the curve?"

- Jerome Powell's Testimony at His Nomination Hearing for a Second Term as Chair of the Board of Governors of the Federal Reserve System; A Link to The Beige Book

- Federal Reserve Chairman Jerome Powell: Monetary Policy in the Time of Covid

- Prices are Spiking for Homes, Cars and Gas; Don’t Be Alarmed, Economists Say

- New Economic Challenges and the Fed's Monetary Policy Review by Chair of the Federal Reserve Jerome H. Powell