September 07, 2022

Bringing Inflation Down

Vice Chair Lael Brainard

At the Clearing House and Bank Policy Institute 2022 Annual Conference, New York, New York

|

||||||||||||||||||||||||||||

|

|

Speech

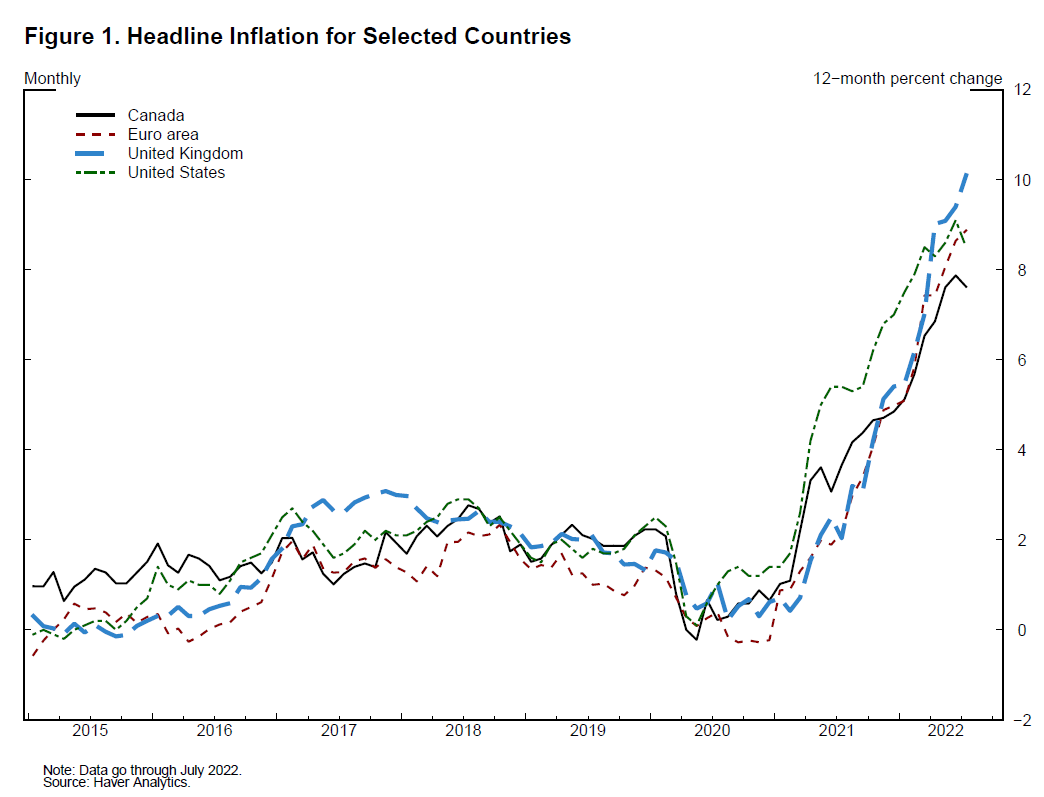

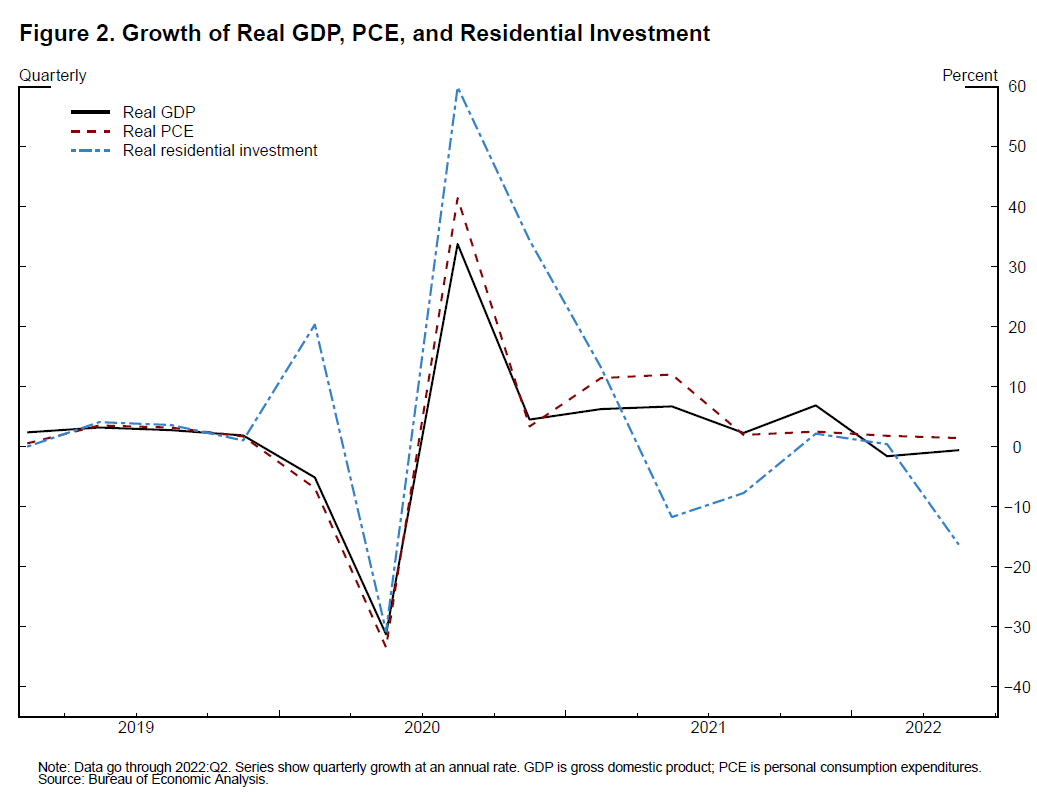

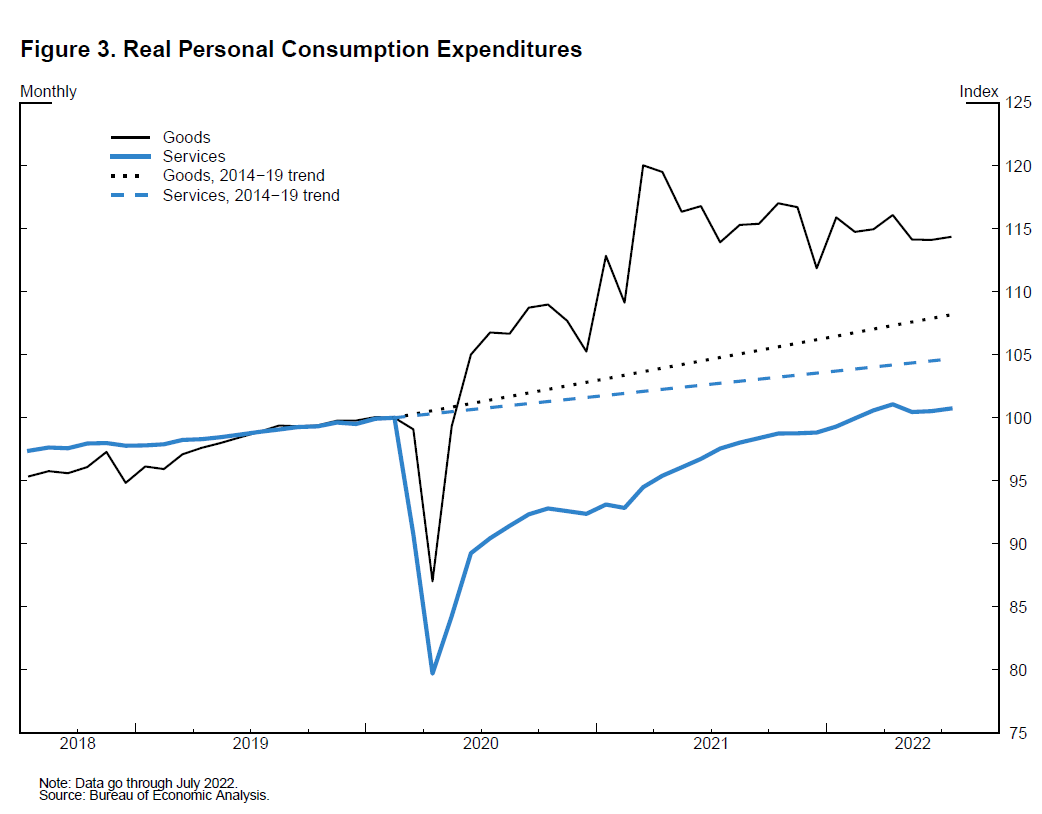

September 07, 2022 Bringing Inflation DownVice Chair Lael Brainard At the Clearing House and Bank Policy Institute 2022 Annual Conference, New York, New York Over the past year, inflation has been very high in the United States and around the world (figure 1). High inflation imposes costs on all households, and especially low-income households. The multiple waves of the pandemic, combined with Russia's war against Ukraine, unleashed a series of supply shocks hitting goods, labor, and commodities that, in combination with strong demand, have contributed to ongoing high inflation. With a series of inflationary supply shocks, it is especially important to guard against the risk that households and businesses could start to expect inflation to remain above 2 percent in the longer run, which would make it much more challenging to bring inflation back down to our target. The Federal Reserve is taking action to keep inflation expectations anchored and bring inflation back to 2 percent over time.1 Photo taken of Brainard at 2019 Federal Reserve System Community Development Research Conference* While last year's rapid pace of economic growth was boosted by accommodative fiscal and monetary policy as well as reopening, demand has moderated this year as those tailwinds have abated. A sizable fiscal drag on output growth alongside a sharp tightening in financial conditions has contributed to a slowing in activity. In the first half of 2022, real gross domestic product (GDP) declined outright, overall real consumer spending grew at just one-fourth of its 2021 pace, and residential investment, a particularly interest-sensitive sector, declined by 8 percent (figure 2).2 The concentration of strong consumer spending in supply-constrained sectors has contributed to high inflation. Consumer spending is in the midst of an ongoing but still incomplete rotation back toward pre-pandemic patterns. Real spending on goods has declined modestly in each of the past two quarters, while real spending on services has expanded at about half its 2021 growth rate. Even so, the level of goods spending remains 5 percent above the level implied by its pre-pandemic trend, while services spending remains 4 percent below its trend (figure 3). In addition to the fiscal drag and tighter financial conditions, high inflation—particularly in food and gas prices—has restrained consumer spending by reducing real purchasing power. While price increases in food and energy are weighing on discretionary spending by all Americans, they are especially hard on low-income families, who spend three-fourths of their income on necessities such as food, gas, and shelter—more than double the 31 percent for high-income households.3 Since the very elevated prices at the pump in June, the nationwide average price of a gallon of regular unleaded gasoline has declined every day throughout July and August, most recently falling below $4 a gallon, according to the American Automobile Association.4 The rise and fall of gasoline prices played a major role in the dynamics of inflation over the summer, contributing 0.4 percentage point to month-over-month personal consumption expenditures (PCE) inflation in June and subtracting 0.2 percentage point in July. This 0.6 percentage point swing in the contribution of gasoline prices was an important driver of the decline in month-over-month PCE inflation from 1 percent in June to negative 0.1 percent in July. In contrast, food price pressures continue to worsen, reflecting Russia's continuing war against Ukraine, as well as extreme weather events in the United States, Europe, and China.5 The PCE index for food and beverages has increased each month this year by an average of 1.2 percent, resulting in an 8-1/2 percent cumulative increase in the index year-to-date through July. For context, the net change in the food and beverages price index over the entire four-year period before the pandemic was only 0.5 percent.

|

|

||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

SeniorWomenWeb, an Uncommon site for Uncommon Women ™ (http://www.seniorwomen.com) 1999-2024

{kind=link}

{kind=link}

{kind=link}